Mixed Signals: A Tough Job Market vs. A Borrower’s Bonanza in the 2025 Economy

If you’re trying to make sense of the U.S. economy in 2025, you might be getting whiplash. Headlines scream about layoffs in one section and celebrate plunging mortgage rates in the next. It feels contradictory because, well, it is. The economy is sending mixed signals, and whether you see a cloud or a silver lining depends entirely on your personal situation.

Let’s break down this strange economic dichotomy and what it means for you.

—

Part 1: The Cloud – Cooling Labor Market Puts Pressure on Workers

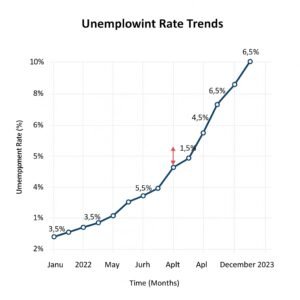

For the past few years, employees held the cards. The “Great Resignation” led to soaring wages and abundant opportunities. But in 2025, the winds have shifted.

What’s Happening? The Federal Reserve’s prolonged battle against inflation has finally cooled the economy down—perhaps a bit too much. Companies, facing higher borrowing costs and cautious consumer spending, are hitting the pause button on hiring. We’re seeing more announcements of layoffs, particularly in the tech and service sectors, and a noticeable rise in the unemployment rate.

What This Means for You:

· Harder Job Hunts: Landing a new role takes longer, and there’s more competition for open positions.

· Slower Wage Growth: The powerful bargaining power employees had is diminishing. Raises might be smaller, and switching jobs for a big pay bump is less of a sure thing.

· Job Insecurity: The fear of layoffs is creeping back into the national conversation for the first time in years.

For workers, this is undoubtedly the “bad news” part of our story. The era of easy job-hopping and giant sign-on bonuses is over for now.

—

Part 2: The Silver Lining – Mortgage Rates Finally Retreat

Now, for the flip side. The very same economic cooling that’s causing job market jitters is directly responsible for some fantastic news for anyone looking to buy a home or refinance.

What’s Happening? The Fed’s primary goal was to tame inflation. With their policy measures working (and the softer job market being evidence of that), they’ve begun to cut the federal funds rate. Mortgage rates, which loosely follow the yield on the 10-year Treasury note, anticipate these moves. They’ve fallen significantly from their painful peaks of over 7% in 2023-2024.

What This Means for You:

· Improved Affordability: Every half-point drop in your mortgage rate can save you hundreds of dollars on your monthly payment and tens of thousands over the life of the loan.

· More Buying Power: Suddenly, the home that was just out of your budget six months ago might now be within reach. This is breathing some life back into the housing market.

· Refinance Opportunities: Homeowners who bought or refinanced when rates were high now have a golden opportunity to lower their monthly expenses.

—

How Can One Economy Produce Both Outcomes?

It seems paradoxical, but it’s all connected through the Federal Reserve’s actions.

High Inflation → Fed Raises Rates → Expensive borrowing cools the economy and the job market → Lower Inflation → Fed Cuts Rates → Cheaper borrowing (including mortgages) stimulates the economy.

We are currently in the transition phase between the “cooling the economy” and “stimulating the economy” parts of that cycle. The job market feels the chill first, while the housing market gets the first taste of the coming warmth.

Navigating the 2025 Economy: Tips for You

So, where does this leave you? It depends on your focus.

If you’re worried about your job:

· Prioritize Stability: Now might not be the time for a risky career move. Focus on solidifying your value in your current role.

· Build Your Emergency Fund: If you don’t have 3-6 months of expenses saved, make it a top priority. This is your buffer against uncertainty.

· Upskill: Use any downtime to learn new skills that make you more indispensable or marketable.

If you’re looking to buy or refinance a home:

· Get Pre-Approved: Connect with a lender to understand exactly how much you can afford at today’s rates.

· Move deliberately, not hastily: Rates are better, but inventory is still low. Be prepared to act, but don’t feel pressured to overpay for a property.

· Run the Numbers: Use online mortgage calculators to see exactly how much a lower rate saves you. The numbers might be motivating!

—

The bottom line: The 2025 economy isn’t easily labeled as “good” or “bad.” It’s a economy in transition. For workers, it’s a time for caution and preparation. For mortgage borrowers, it’s a window of opportunity that’s finally opening after a long wait. By understanding the forces at play, you can make smart financial decisions no matter which side of the divide you’re on.

—

What’s your take? Are you feeling the pinch of the job market or excited about lower mortgage rates? Share your story in the comments below!

—

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Please consult with a financial professional for advice tailored to your specific situation.