What is HELOC and is it for you?

The HELOC Handbook: Is Tapping Your Home’s Equity a Smart Move?

You’ve been paying your mortgage faithfully for years. You’ve watched your home’s value climb. Now, that financial effort is sitting silently in your house in the form of home equity. It’s a powerful asset, and a Home Equity Line of Credit (HELOC) is one of the most popular tools to unlock it. But is it the right tool for you?

Let’s break down what a HELOC is, how it works, and the critical pros and cons to consider before you sign on the dotted line.

What Exactly is a HELOC?

Think of a HELOC as a hybrid between a credit card and a mortgage.

· It’s a Line of Credit: Like a credit card, you are approved to borrow up to a certain limit. You can withdraw money as you need it, pay it back, and borrow again during the “draw period.”

· It’s Secured by Your Home: Unlike a credit card, this loan uses the equity in your home as collateral. This makes it less risky for the lender, which usually means a lower interest rate for you.

Your equity is simply your home’s current market value minus the amount you still owe on your mortgage.

Equity = Home’s Current Value – Remaining Mortgage Balance

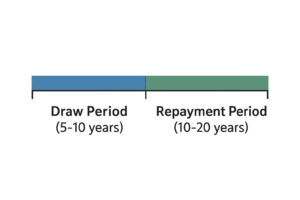

How a HELOC Works: Two Distinct Phases

A HELOC’s life cycle is split into two main phases:

1. The Draw Period (Typically 5-10 years):

· During this time, you can access your funds by writing checks or using a special card linked to the account.

· You usually only have to make interest-only payments on the amount you’ve withdrawn. This keeps initial payments low.

· You can pay down the balance and re-borrow the funds, giving you flexible, revolving access to cash.

2. The Repayment Period (Typically 10-20 years):

· Once the draw period ends, the “door” to borrowing more money closes.

· You can no longer withdraw funds.

· You must now make regular monthly payments that cover both principal and interest to pay off the entire balance over the remaining term.

The Allure: When a HELOC is a GREAT Idea

HELOCs are fantastic for specific, value-driven purposes:

· Home Improvements: This is the classic and best use. Using a HELOC to renovate your kitchen, add a bathroom, or replace a roof can actually increase your home’s value, potentially giving you a return on your investment.

· Debt Consolidation: If you have high-interest debt (like credit cards or personal loans), you can use a HELOC’s lower interest rate to pay them off. Warning: This only works if you have the discipline to not run your credit cards back up again.

· Emergency Fund: It acts as a powerful safety net for unexpected major expenses, like a medical emergency or urgent major repair (e.g., a new furnace).

The Pitfalls: When a HELOC is a RISKY Idea

Tapping your home’s equity is serious business. Avoid using a HELOC for:

· Discretionary Spending: Financing a vacation, a wedding, or a new boat with your house as collateral is extremely risky. These purchases provide no financial return and leave you with debt secured by your most important asset.

· Routine Expenses: If you need a HELOC to cover monthly bills, it’s a sign of a deeper budget problem. This can quickly lead to a dangerous debt spiral.

· Speculative Investments: Do not use a HELOC to invest in the stock market or crypto. Investments can lose value, but your HELOC payment will remain, putting your home at risk.

The Biggest Risks You MUST Understand

1. Your Home is on the Line: This is the #1 rule. If you fail to make your payments, the lender can foreclose on your home.

2. Variable Interest Rates: Most HELOCs have variable rates tied to the Prime Rate. If interest rates rise (as they have recently), your monthly payments will too, which can strain your budget.

3. The Payment Shock: The transition from interest-only payments during the draw period to larger principal-and-interest payments during the repayment period can be a nasty surprise if you aren’t prepared.

4. The Temptation to Overspend: The easy access to a large sum of money can lead to impulsive spending and deeper debt.

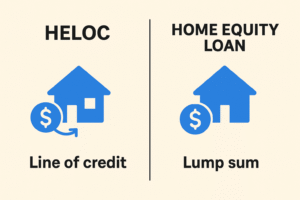

HELOC vs. Home Equity Loan: What’s the Difference?

· HELOC: Icon of a credit card. Label: “Line of Credit.” Subtext: “Variable Rate, Flexible Access.”

· Home Equity Loan: Icon of a check. Label: “Lump Sum.” Subtext: “Fixed Rate, Fixed Payments.”

People often confuse these two. A Home Equity Loan gives you a lump sum of cash all at once, with a fixed interest rate and fixed monthly payments. A HELOC is a revolving credit line with a variable rate. Choose a loan for a one-time, known expense (like a specific roof quote). Choose a HELOC for ongoing or uncertain costs (like a multi-phase renovation).

The Bottom Line: Is a HELOC Right for You?

Ask yourself these questions:

· Do I have a stable income and a strong credit score?

· What is my specific, financial purpose for this money? (Is it an investment or an expense?)

· Do I have the discipline to use it responsibly and not like free cash?

· Am I comfortable with the risk that my home is the collateral?

· Can I handle the payment if interest rates go up?

Final Thought: A HELOC is a powerful financial lever. Used wisely for value-added projects or debt management, it can be a brilliant tool. Used carelessly for wants instead of needs, it can jeopardize the roof over your head. Always consult with a financial advisor to see if it aligns with your overall financial plan.

—

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Please consult with a qualified financial professional before making any decisions regarding a HELOC