Your Ultimate Guide to Building a Killer Credit Score in Your 20s

Hey there, future financial rockstar!

Let’s talk about your credit score. I know, I know—it sounds about as exciting as watching paint dry. But stick with me. This little three-digit number is like a financial passport. A great score (generally 670+) will unlock the best interest rates on car loans, help you get that sweet apartment, and eventually, save you tens of thousands of dollars on a mortgage.

The best part? Building it is a game of consistency, not complexity. And starting young gives you the biggest advantage of all: time.

So, let’s break it down into simple, actionable steps.

—

Step 1: The Foundation – Understand What a Credit Score Is

Before you build it, you need to know what “it” is.

Your credit score is a number that represents your “creditworthiness”—basically, how likely you are to pay back money you borrow. It’s calculated based on the information in your credit reports at the three major bureaus: Experian, Equifax, and TransUnion.

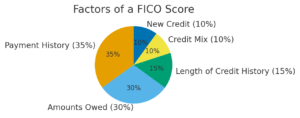

The most common scoring model is FICO, which is made up of five components:

· Payment History (35%): The most important factor. Do you pay your bills on time?

· Amounts Owed/Credit Utilization (30%): How much of your available credit are you using?

· Length of Credit History (15%): How long have you had your accounts?

· Credit Mix (10%): Do you have a mix of credit types (e.g., credit card, student loan)?

· New Credit (10%): How many new accounts or hard inquiries do you have?

—

Step 2: Check Your Credit Report (It’s Free!) Click here for your free credit report

You can’t manage what you can’t see. You are entitled to a free credit report from each of the three bureaus every week at AnnualCreditReport.com.

Always use the official, free website to get your reports.

What to do:

1. Go to the website and request your reports.

2. Scan them for errors—wrong personal info, accounts you didn’t open, or incorrect late payments.

3. If you find a mistake, dispute it directly with the credit bureau. This is crucial for maintaining an accurate score.

—

Step 3: Get Your First Credit Card

If you have no credit history, you have to start somewhere. This is the most common first step.

Options for your first card:

· Secured Credit Card: This is the #1 tool for building credit from scratch. You provide a cash deposit (e.g., $200) that usually becomes your credit limit. You use it like a normal card, and the issuer reports your payments to the credit bureaus. After 6-12 months of on-time payments, you can often “graduate” to an unsecured card and get your deposit back.

· Student Credit Card: If you’re in college, these are designed for you. They often have lower credit requirements and may offer rewards on things like dining or streaming services.

· Become an Authorized User: A parent or trusted family member can add you to their existing credit card account. Their positive payment history can help build your score. Proceed with caution: Their mistakes can also hurt your score, so only do this with someone who is extremely responsible.

—

Step 4: Use Your Card the RIGHT Way

This is where the magic happens. Getting the card is easy. Using it wisely is the key.

The Golden Rules:

1. Pay On Time, EVERY Time. Set up autopay for the statement balance to ensure you never, ever miss a payment. Payment history is 35% of your score!

2. Keep Your Utilization LOW. This is the #1 mistake beginners make. Credit utilization is how much you owe compared to your limit. Aim to use less than 30% of your limit, and under 10% is ideal. For a $1,000 limit, try not to have a balance higher than $300 when the statement closes.

· Pro Tip: You can pay down your balance before your statement closing date to keep your reported utilization super low.

3. Don’t Chase Rewards. Your goal is building credit, not earning points yet. Spend only on what you can afford to pay off immediately. A credit card is a tool, not free money.

—

Step 5: Diversify and Let It Age

Once you’ve had your first card for 6-12 months and have a history of on-time payments, you can think about the long game.

· Keep Old Accounts Open: The length of your credit history matters. That first crummy secured card you got? Keep it open (even if you don’t use it much) to lengthen your average account age.

· Consider a Credit-Builder Loan: Some banks and credit unions (or services like Self) offer these. You make fixed payments into a savings account, and once the “loan” is paid off, you get the money back. It’s a forced savings plan that also adds a different type of credit (installment loan) to your mix.

—

Step 6: Monitor and Stay the Course

Building excellent credit is a marathon, not a sprint.

· Use free services from your bank or like Credit Karma or Experian to monitor your score and get alerts.

· Continue practicing good habits: pay everything on time, keep balances low, and only apply for new credit when you need it.

.

.

The Bottom Line

Your credit score is a reflection of your financial habits. By starting young and being consistent, you’re not just building a number—you’re building a foundation for a life of financial freedom and opportunity.

Your action plan:

1. Pull your free credit reports.

2. Research and apply for a secured or student card.

3. Use it for one small, recurring subscription.

4. SET UP AUTOPAY.

5. Watch your score grow!

What’s your biggest question about credit scores? Drop it in the comments below!